The Philippine tax system is like a tool that helps the country run smoothly. It collects money for important things like roads, schools, hospitals, and programs that help people. If you live, work, or invest in the Philippines, it’s important to understand how taxes work. This guide will explain the different kinds of taxes, who’s in charge of collecting them, and how you can ensure you’re paying the right amount of tax.

The Philippine Tax System

The Philippine tax system collects money for the government, which is used to pay for things like the army, hospitals, roads, and schools. Taxes are not only about making money. They can also help balance the country’s wealth, control certain businesses, and boost the economy.

Importance of the Tax System

| • | Revenue Generation: Taxes are like the money a government needs to function. With taxes, important services and infrastructure like roads, public schools, and hospitals stay open, which could help improve the economy. |

| • | Economic Stability: Taxes can help control prices and influence how people spend money, helping the economy steady. |

| • | Social Equity: Taxes can ensure everyone has a fair share of money. People who earn more might have to pay a higher percentage of their income in taxes, which can help balance things out. |

Brief History of the Philippine Tax System

The Philippine tax system has a long history. It started with simple taxes for local leaders before the Spanish came. When the Spanish arrived, they introduced new taxes like the “tributo” and the “cedula.” After the Philippines became independent, the tax system was changed to fit a growing country.

Objectives of the Tax System

| • | Promote Economic Growth: By funding infrastructure and public services. |

| • | Ensure Social Equity: Through a progressive tax system that taxes higher-income earners more. |

| • | Regulate Economic Activity: Taxes can encourage good things and discourage bad things. For example, taxes on alcohol and cigarettes can help reduce their use, while tax breaks for renewable energy can encourage people to use clean energy. |

Understanding the Philippines’ tax system’s purpose and history can empower taxpayers to comply more meaningfully. It helps citizens recognize taxation as a legal duty and a crucial investment in a stable and prosperous nation.

Types of Taxes in the Philippines

There are three main types of taxes in the Philippines: direct, indirect, and local. Each type has different rules and is used for various purposes. It’s important for everyone, from individuals to businesses, to understand these taxes to make sure they follow the tax laws and manage their money well.

A. Direct Taxes

Direct taxes are like taxes you pay directly on the money you make or the things you own. People who earn more usually have to pay a higher percentage of their income in taxes. This is called a progressive tax system.

1. Income Tax

This tax is calculated based on all the money you make in a year. You’re usually responsible for determining how much tax you owe based on your income level. The exemptions are listed on the BIR Income Tax Return page.

Types of Income Tax and Sub-Categories

In the Philippines, income tax can be divided into several types, depending on who pays the tax and how the income is earned. Below are the different income tax types and their sub-categories.

i. Individual Income Tax

This is the tax paid by individuals, including employees, professionals, freelancers, and self-employed people, on their earnings. The amount of tax depends on the individual’s income level. There are two main sub-categories:

a. Employee (Salaried Individuals): Employees working for companies or the government pay income tax on their salaries. Taxes are usually deducted automatically from their paychecks through the Withholding Tax System.

b. Self-Employed and Professionals: Individuals running their businesses or working as freelancers and consultants also pay income tax on their earnings. They must file and pay taxes independently.

ii. Corporate Income Tax

This is the tax paid by corporations or businesses on their profits. There are several sub-categories within corporate income tax:

a. Regular Corporate Income Tax (RCIT): A standard tax rate applied to the taxable income of corporations. Domestic corporations are taxed on their global income, while foreign corporations are taxed only on income earned in the Philippines. This tax is usually 25%, but it can be lowered to 20% for smaller companies. The profit is calculated by subtracting expenses from the total money they earned.

b. Minimum Corporate Income Tax (MCIT): A tax applied to corporations when their regular income tax is lower than 2% of their gross income. It’s a way to ensure that corporations pay at least some taxes even in years when they report minimal profits.

c. Special Corporate Tax Rates: Certain businesses, like those in special economic zones or those registered with the Philippine Economic Zone Authority (PEZA), may qualify for lower or preferential tax rates.

If a company exports products or services from the Philippines, it might get a tax break for a few years. This is called an Income Tax Holiday (ITH). The length of the tax holiday depends on where the company is located and what kind of business it is.

After the ITH ends, these companies can choose between two options for the next 10 years:

| 5% Special Corporate Income Tax (SCIT): | They pay a lower tax rate of 5% on their total income. |

| Enhanced Deductions: | They can deduct more expenses from their income before calculating taxes. |

If they choose the 5% SCIT option, they need to pay:

| • | 3% to the national government |

| • | 2% to the local government where their business is located |

This means the company pays 5% of total corporate income tax.

iii. Withholding Tax

Withholding tax is a type of income tax that pre-pay income taxes. There are different sub-categories of withholding tax that are deducted at the source of income:

a. Expanded Withholding Tax (EWT): Tax withheld from certain payments like professional fees, rentals, or commissions. This is usually done within 10 days after you withhold the taxes. If you’re a big company, you must file and pay by the 25th day of the following month.

b. Final Withholding Tax (FWT): Tax withheld on certain types of income like interest (20%), dividends (15%-25%), and royalties (20%-25%). The tax withheld is considered final, meaning the payee no longer needs to file additional income tax on that income.

c. Compensation Withholding Tax: This applies to employees where employers deduct income tax from their salary and remit it to the government on their behalf. You can use the BIR Withholding Tax Calculator to calculate the correct amount of withholding tax for earnings, services, or other income. The specific details you provide on this online tool will automatically calculate the tax.

iv. Capital Gains Tax

This is a tax on the profit made from selling assets like real estate or shares of stock. There are two sub-categories:

a. Capital Gains Tax on Real Estate: A tax imposed when someone sells real estate property. The rate is typically 6% of the sale price, zonal value, or the fair market value, whichever is higher.

| Who pays the CGT? Generally, the buyer or transferee of the asset is responsible for withholding the CGT from the seller and remitting it to the government. When you sell a property, the buyer will typically deduct the CGT from the selling price and pay it to the tax authorities on your behalf. |

b. Capital Gains Tax on Shares of Stock: If someone sells stock shares not listed on the stock exchange, they need to pay a 15% tax on the profit.

v. Fringe Benefits Tax

This is a tax on employees’ benefits that are not part of their regular salary, such as housing, cars, or expense accounts. The employer is responsible for paying this tax, which is 35% of the value of the benefits provided.

Tax Rates for Individuals and Corporations

Individual Tax Rates: Under the TRAIN Law, individuals are taxed based on a progressive scale:

| Taxable Income | Tax Rate |

| ₱0 – ₱250,000 (US$4,279) | 0% |

| ₱250,001 – ₱400,000 (US$4,279)-(US$6,848) | 20% of the excess over ₱250,000 |

| ₱400,001 – ₱800,000 (US$6,848)-(US$13,697) | ₱30,000 + 25% of the excess over ₱400,000 |

| ₱800,001 – ₱2,000,000 (US$13,697)-(US$34,242) | ₱130,000 + 30% of the excess over ₱800,000 |

| ₱2,000,001 – ₱8,000,000 (US$34,242)-(US$136,972) | ₱490,000 + 32% of the excess over ₱2,000,000 |

| Above ₱8,000,000 (US$136,972) | ₱2,410,000 + 35% of the excess over ₱8,000,000 |

Courtesy of ASEAN Briefing: Ayman Falak Medina, July 16, 2024

| The TRAIN Law: Republic Act No. 10963: The Tax Reform for Acceleration and Inclusion or TRAIN 1, is a new tax law passed in the Philippines in 2017. It aimed to make the tax system easier to understand, fairer, and more efficient. The goal was to collect more taxes that could be used for things like building roads and bridges, helping people in need, and improving education and healthcare. |

Tax Brackets and Exemptions

There are several exemptions you can claim on your income tax return. These exemptions can help you pay less tax by reducing your taxable income. Some common exemptions include:

| • | Basic Personal Exemption: A standard deduction, or a fixed amount you can subtract from your taxable income. The amount depends on your filing status: single, married, or have children. If you’re filing taxes as a single person, you can subtract PHP 50,000 from your taxable income. If you’re married and only one works, that person can claim the PHP 50,000 deduction. |

| • | Additional Exemptions: If you have children, you might get an extra deduction on your income tax. For each child you have (up to four), you can subtract PHP 25,000 from your taxable income. Usually, the father claims this deduction, but he can let the mother claim it instead. |

| • | Professional Fees: If you pay for professional services like accountants, lawyers, or doctors, you may deduct those costs from your income before calculating your tax. This means you’ll pay less tax. |

| • | Contributions: If you donate money to charities or government-approved retirement plans, you can deduct those contributions from your income. This can also help you pay less tax. |

If you’re a business owner or professional, you can either itemize your deductions or use a simplified deduction method. You need to indicate your choice on your tax return. Once you choose, you can’t change it for that tax year. If you don’t select one, it’s assumed you’ve opted to itemize your deductions.

i. Itemized Deductions

Itemized deductions are like discounts you can use to pay less income tax. They’re specific expenses you can subtract from your total income. Some examples include interest on loans, taxes you paid, losses from investments, and money you donated to charities.

What are some common itemized deductions?

| Interest: | Interest paid on loans or debts. |

| Taxes: | Property taxes, sales taxes, or other taxes you paid. |

| Losses: | Losses from business or investments. |

| Bad Debts: | The money you lent to others that you couldn’t collect. |

| Depreciation: | The decrease in the value of assets over time. |

| Depletion: | The decrease in natural resources over time. |

| Charitable Donations: | The money you gave to charities. |

| Research and Development: | Costs for research and development. |

| Pension Trust: | Contributions to retirement plans. |

| Health Insurance: | Premiums you paid for health or hospitalization insurance. |

ii. Health Insurance Deduction:

You can deduct up to PHP 2,400 per year for health insurance premiums for yourself and your family if your combined yearly gross income is less than PHP 250,000. If you’re married, only the spouse claiming the additional exemption for dependents can claim this deduction.

| Remember: You can either itemize your deductions or take a standard deduction. The specific deductions you can use and the rules might change, so it’s best to ask a tax expert for the latest information. |

2. Estate Tax

Imagine you have a relative who passed away. They leave behind a house, a car, and some money. Estate tax is like a fee that the government charges on these things. It’s a tax on the property that someone leaves behind when they die.

Here’s a breakdown:

| • | Direct Tax: It’s a tax on the person who owned the property, not on the property itself. |

| • | Triggered by Death: Estate tax only happens when the owner dies. |

| • | Fair Market Value: The tax is based on how much the property is worth today, not how much it cost originally. |

An estate tax is a way for the government to collect money when someone dies and leaves behind property.

Key Components of Estate Tax in the Philippines under TRAIN Law

Estate Tax Rate: Established by the TRAIN Law the current estate tax rate is 6% of the net estate value. This means that for every PHP 100 of estate value, you’ll pay PHP 6 in taxes.

i. Gross Estate

The estate tax is based on the total value of everything the deceased person owns. This includes houses, cars, money in the bank, investments, life insurance, businesses, and even things like patents or copyrights. The government adds the value of all these things to know how much tax is owed. Here’s a breakdown of what gets counted as gross estate:

| • | Assets you own outright: This includes things like your house, car, bank accounts, investments, and any valuable personal property (like a coin collection or artwork). |

| • | Things you had a share in: If you owned part of a business, or jointly owned property with someone else (like a house with your sibling), the value of your share is counted towards the estate tax. |

| • | Gifts you gave away shortly before you died: This is to prevent people from giving away all their assets to their heirs just before they die to avoid taxes. There are rules about how long before you die you need to give something away for it to be excluded from your estate tax. |

| • | Life insurance money: Generally, if you had a life insurance policy and the money goes to your estate (the pool of all your assets after you die) or to named beneficiaries you can change at any time, the payout is counted towards your estate tax. There’s an exception if you name a beneficiary who can’t be changed, such as a trust. |

| • | Things you could control, even if you didn’t own them outright: This applies to trusts or other situations where you decide who inherited something after you died, even if it wasn’t technically yours on paper. |

| Important exceptions to remember: Money and property of your surviving spouse: Generally, your spouse inherits your assets tax-free. The marital deduction is calculated at 50% of the net estate of the deceased spouse. Things you sold for a fair price: If you sold something close to its actual market value during your lifetime, the money you received doesn’t count towards your estate tax. This is to avoid taxing you on money you no longer own. |

ii. Net Estate

The net estate is calculated by subtracting allowable deductions from the gross estate. These deductions include:

| • | Standard Deduction: A fixed amount (PHP 5 million for residents, PHP 500,000 for non-residents). |

| • | Claims Against the Estate: Debts owed by the deceased. |

| • | Unpaid Mortgages: Loans secured by property. |

| • | Property Previously Taxed: Property that was already taxed when it was given to the deceased. |

| • | Transfers for Public Use: Donations to the government. |

| • | Family Home: Up to PHP 10 million. |

| • | Amounts Received Under Republic Act No. 4917: Certain amounts received by heirs from the decedent’s employees. |

| • | Surviving Spouse’s Share: The surviving spouse’s share of conjugal property. |

| • | Foreign Tax Credits: Taxes paid to foreign governments. |

Estate Tax Returns

Estate Tax Returns are documents filed with the government to report the value of a deceased person’s estate and calculate the amount of estate tax owed. These returns provide the tax authorities with information about the deceased person’s assets, debts, and beneficiaries. (See BIR Form No. 1801 guidelines).

Here’s what you need to know:

| • | Filing a Return: The person in charge of settling the estate (usually a family member) files a tax return. |

| • | Providing Information: The return must include details about the person’s assets, debts, and any money they gave away before they died. |

| • | Supporting Documents: The return may need to be accompanied by supporting documents, such as a death certificate, inventory of assets, proof of ownership, copies of life insurance policies, receipts for funeral expenses, bank statements, investment records, deeds, titles, and extrajudicial settlements (if applicable). |

| • | Large Estates: If the estate is worth more than PHP 5 million, you’ll need to provide extra information and get a certified accountant to help you with the return. |

| • | Tax Calculation: The tax authorities will use the information in the return to calculate the estate tax liability based on the applicable tax rates and deductions. |

| • | Deadline: You generally have one year after the person dies to file the return. |

| • | Extensions: In some cases, you can get an extension of up to 30 days to file the return. |

| • | Where to File: To file the estate tax return, you must go to a bank authorized to handle tax payments. The specific bank will depend on where the deceased person lived. |

| • | Payment of Tax: The estate tax is usually paid when you file the tax return. If you can’t pay the full amount at once, you might be able to pay it in smaller amounts over two years, but you’ll need permission from the tax office. |

| • | Penalties and Interest: If you don’t file the return on time or don’t pay the full amount, you might be charged a penalty of 25% of the amount due or interest equivalent to 20% annually. |

| Remember: It’s important to consult with a tax professional for personalized advice and assistance navigating the estate tax process. They can help ensure you comply with all applicable laws and regulations and minimize your estate tax liability. |

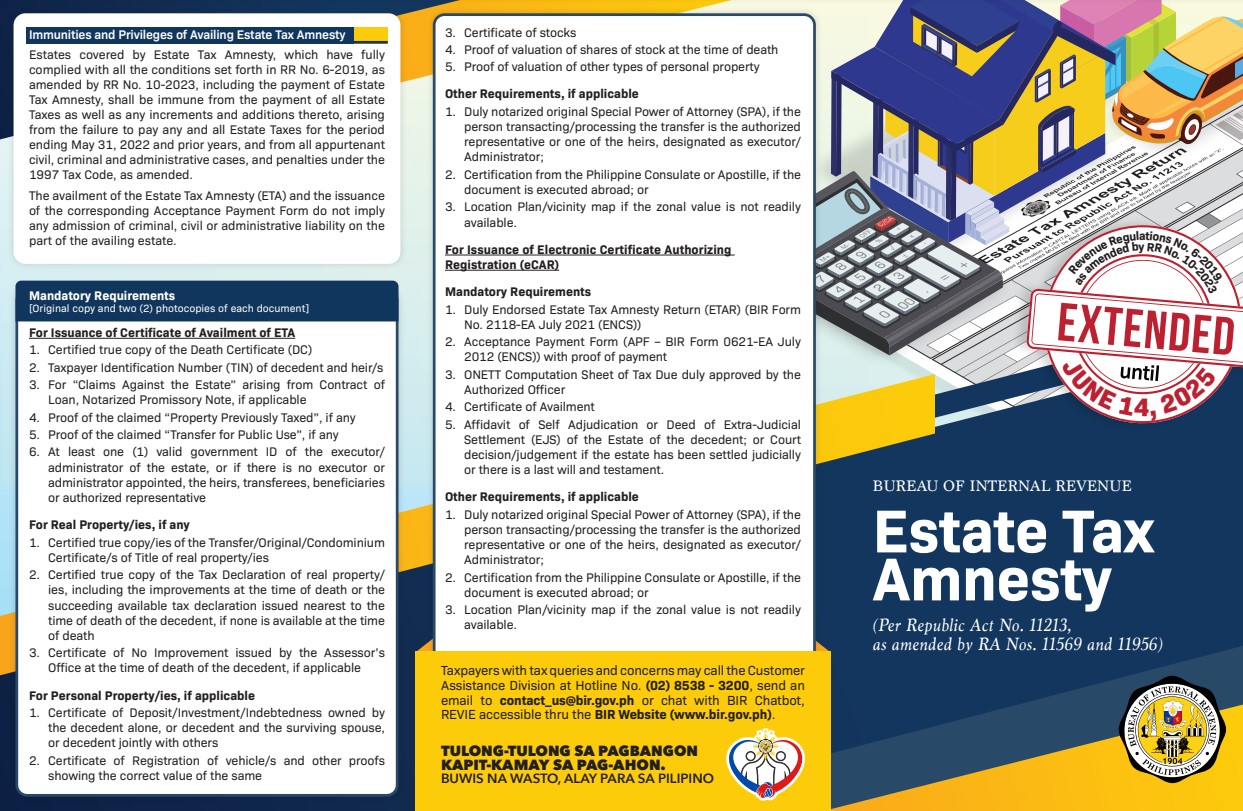

What is an Estate Tax Amnesty?

An estate tax amnesty is a government program that offers reduced penalties or exemptions for taxpayers who voluntarily declare and pay their estate taxes. These programs are typically implemented to encourage tax compliance and increase government revenue.

Estate Tax Amnesty in the Philippines

Estates that have fully complied with the requirements of Revenue Regulations Nos. 6-2019 and 10-2023, including the payment of estate tax amnesty, shall be granted immunity from all estate taxes, increments, additions, civil, criminal, and administrative cases, and penalties arising from non-payment of estate taxes for the period ending May 31, 2022, and prior years.

Estate Tax Amnesty Program

This program allows estates that didn’t pay their estate taxes on time to avoid penalties. If you qualify, you can pay a reduced amount and avoid legal trouble.

| Who Qualifies: | • Estates of people who died before May 31, 2022, even if they haven’t been assessed for taxes yet. |

| • Estates that haven’t paid any estate taxes for the period ending May 31, 2022. |

| Deadline: | • You must apply for the amnesty by June 14, 2025. |

| Required Documents | |

| For the Certificate of Availment: | • A copy of the death certificate. |

| • Taxpayer ID numbers for the deceased and their heirs. | |

| • If applicable: proof of loans, property previously taxed, or donations to public causes. | |

| • Government ID for the executor, administrator, or representative. | |

| For Real Property: | • Property title or ownership documents. |

| • Tax declarations for the property. | |

| • Certificate of No Improvement (if applicable). | |

| For Personal Property: | • Bank statements, vehicle registration, stock certificates, etc. |

| • Proof of valuation for shares or other property. | |

| Other: | • Special Power of Attorney (if applicable) |

| • Certification from the Philippine Consulate (if documents were created abroad) | |

| • Location map (if property value can’t be determined easily) | |

| For the Electronic Certificate Authorizing Registration (eCAR): | • Estate Tax Amnesty Return (ETAR) |

| • Acceptance Payment Form (APF) | |

| • ONETT Computation Sheet | |

| • Certificate of Availment | |

| • Affidavit of Self-Adjudication or Deed of Extra-Judicial Settlement (EJS) | |

| • Special Power of Attorney (if applicable) | |

| • Certification from the Philippine Consulate (if applicable) | |

| • Location map (if applicable) |

| Remember: The estate tax amnesty doesn’t mean you’re admitting wrongdoing. However, the rules might change, so it’s best to check with the tax office for the latest information. There might be a fee to apply, and a tax professional can help make the process easier. |

3. Donor’s Tax

Donor’s Tax is a tax on giving someone else property as a gift. It applies to everyone, whether they live in the Philippines or not, and whether the gift was given directly or through a trust. The tax is based on the value of the gift.

Tax Rates on Donations:

| • | More than PHP 250,000: If you give someone a gift worth more than PHP 250,000 in a year, you’ll pay a 6% tax. |

| • | Gifts for Less Than Full Value: If you give someone a gift worth more than it cost you, the difference is considered a gift and will be taxed. However, if you sell something for a fair price, it’s not considered a gift. |

i. Gifts That Aren’t Taxed

a. If you’re a Filipino giving a gift, you don’t have to pay tax on these things:

| • | Gifts to the Philippine government or its agencies. |

| • | Gifts to charities, schools, or other non-profit organizations that use at least 70% of the money for their mission. |

b. If you gave a gift to someone in another country and paid taxes on it, you can get a tax break in the Philippines.

| • | The tax break from the foreign country should be smaller than the tax you owe in the Philippines for the same gift. |

| • | The amount of the tax break depends on how much of the gift was in the Philippines compared to other countries. |

| • | To claim this tax break, you need proof of the paid taxes in the other country. |

c. If you’re not a Filipino, you can only get these exemptions if:c

| • | you give the gift to a Philippine government agency; or, |

| • | a non-profit organization in the country. |

ii. Valuation of Gifts Made in Property

If you give someone a property, like a house or land, as a gift; the value of that property at the time you gave it is the amount you’ll be taxed on. To find the value, you can use the same rules for valuing property when someone dies.

Donor’s Tax Return

A Donor’s Tax Return is a document filed with the government when you give someone a gift that is subject to taxation. (See BIR Form No. 1800 guidelines).

Here’s what you need to know:

| • | When to File: You must file the return within 30 days of giving the gift. |

| • | What to Include: The return needs information about the gift, any deductions you can claim, and the person you gave it to. |

| • | Where to File and Pay: You can file the return and pay the tax at a bank that’s authorized to handle tax payments. |

B. Indirect Taxes

Indirect taxes are taxes added to the price of things you buy. Businesses usually pass these taxes on to customers, so the customers are paying these taxes.

1. Value-Added Tax (VAT)

Value-Added Tax (VAT) is a tax added to the price of items you buy. It’s collected at every step, from when something is made to when it’s sold to you. It’s a big source of money for the government.

How VAT Works

| • | Each stage of production or distribution: VAT is added to the price of things at every step, from when they’re made to when they’re sold to you. |

| • | Input Tax vs. Output Tax: Businesses can subtract the VAT they paid for things they bought (input tax) from the VAT they collected from selling things (output tax). |

| • | Net Tax Payable: The net VAT you owe is the difference between the VAT you collected from selling things and the VAT you paid for things you bought. |

VAT Rates

Value-Added Tax (VAT) in the Philippines is generally levied at a standard rate of 12%. But some things, like food, medicine, and exports, have a lower tax or no tax at all.

i. Standard Rate (12%)

Most goods and services: As mentioned earlier, the standard VAT rate is 12% for most goods and services. This includes items like:

| • | Food and beverages (except for essential items) |

| • | Clothing and footwear |

| • | Electronics and appliances |

| • | Automobiles and other vehicles |

| • | Construction services |

| • | Professional services (e.g., legal, accounting) |

ii. Zero Rate (0%)

a. Exports: Goods and services exported from the Philippines are subject to a zero VAT rate. This means that exporters can claim a full refund of the VAT paid on their purchases and inputs.

b. Essential goods: Certain basic goods and services deemed essential for daily living, such as rice, corn, and medicines, may be subject to a zero VAT rate.

Exempt Goods and Services

| • | Financial services: Banking, insurance, and other financial services are generally exempt from VAT. |

| • | Health care services: Hospital services, medical consultations, and prescription drugs are typically exempt from VAT. |

| • | Educational services: Tuition fees and other educational services are usually exempt from VAT. |

| • | Government services: Services provided by the government are generally exempt from VAT. |

| • | Certain agricultural products: Some agricultural products, such as unprocessed agricultural food, may be exempt from VAT. |

| • | Religious activities: Religious services and activities are typically exempt from VAT. |

| Revenue Regulations No. 1-24: The government has increased the price limit for houses and other homes not subject to VAT. Starting in 2024, homes that cost less than PHP 3,600,000 will not have VAT added to their price. Before, the limit was PHP 3,199,200. |

To get a 0% VAT rate for services, you need to meet these conditions:

| • | The service you’re providing is not about making or changing products. |

| • | You’re providing the service in the Philippines. |

| • | The person you’re providing the service to is a business located outside the Philippines or a person who doesn’t live in the Philippines and isn’t running a business there. |

| • | The payment for the service is made in a foreign currency and reported to the Bangko Sentral ng Pilipinas. |

Monthly Value-Added Tax Declaration

Monthly VAT returns must be filed by all registered taxpayers, regardless of whether they have engaged in taxable transactions or exceeded the VAT registration threshold. This requirement remains in effect until the VAT registration is formally canceled.

Quarterly Value-Added Tax (VAT) Return

The VAT return must be filed within 25 days after the end of each quarter. A quarter is 3 months, depending on whether your business year is based on the calendar (January to December) or a different period (e.g., April to March). (See BIR Form No. 2500Q guidelines).

2. Excise Tax

Excise Tax is a tax imposed on the production, sale, or consumption of specific goods and services. It’s a type of indirect tax, meaning it’s passed on to consumers through higher prices.

Key Points:

| • | Excise tax is a tax on specific goods and services. |

| • | It can be based on weight, volume, or value. |

| • | Different types of products have different excise tax rates. |

| • | The person responsible for paying the tax depends on the product and the transaction. |

| • | The tax is usually paid before the product is sold or used. |

Types of Excise Tax

| • | Specific Tax: Tax based on weight, volume, or other physical unit. |

| • | Ad Valorem Tax: Tax based on the selling price or value of the product. |

Excisable Articles

| • | Alcohol Products: Distilled spirits, wines, fermented liquors |

| • | Tobacco Products: Cigarettes, cigars, tobacco |

| • | Petroleum Products: Gasoline, diesel, kerosene, etc. |

| • | Miscellaneous Articles: Automobiles, non-essential goods, sweetened beverages |

| • | Mineral Products |

Persons Liable for Excise Tax

| • | Domestic Articles: Manufacturers, producers, owners, doctors (for cosmetic procedures) |

| • | Imported Articles: Importers, owners, and persons possessing tax-exempt products illegally |

| • | Indigenous Petroleum: First buyers, purchasers, or transferees for local sale, barter, or transfer; owners, lessees, or operators for exportation |

Time of Payment

Excise tax is usually paid before the product is taken from the factory or released from the customs office. However, there are exceptions for certain types of businesses or products. Some businesses might pay the tax at regular intervals, or in advance. For metallic minerals, the tax must be paid within 15 days after the end of each quarter.

3. Documentary Stamp Tax

Documentary Stamp Tax (DST) is a tax on document transactions like contracts and deeds. It’s like a fee you pay when you sign a legal document.

Types of Documents Subject to DST

| • | Contracts: Sale, lease, exchange, partnership, agency, etc. |

| • | Deeds: Deeds of sale, donation, exchange, mortgage, etc. |

| • | Loans: Promissory notes, mortgage contracts, etc. |

| • | Leases: Lease agreements for real property or personal property. |

| • | Instruments: Bills of exchange, checks, drafts, etc. |

| • | Other documents: Various other documents specified in the Tax Code, such as insurance policies, receipts, and licenses. |

Documentary Stamp Tax (DST) Rates

The DST rate varies depending on the type of document or transaction. It is typically computed based on the value or amount involved in the document or transaction. For example, the DST rate for a deed of sale of real property may be based on the selling price of the property.

Examples of documentary stamp tax rates include:

| • | Contracts of Sale: PHP 15 for the first PHP 1,000 of the consideration. |

| • | Mortgage or Pledge of Lands, Estate, or Property and Deeds of Trust: The tax for mortgages and pledges on property is PHP 40 for the first PHP 5,000. For every additional PHP 5,000 or part thereof, the tax is PHP 20. |

| • | The tax for leases and rental agreements: PHP 6 for the first PHP 2,000 or part thereof. PHP 2 for each additional PHP 1,000 or part thereof, for each year of the lease. |

Documentary Stamp Tax (DST) Exemptions

Certain documents and transactions may be exempt from DST, such as:

| • | Insurance policies from fraternal societies or cooperatives. |

| • | Papers from government officials about oaths or acknowledgments. |

| • | Legal papers filed by government officials. |

| • | Affidavits of poor people. |

| • | Statements and information required by the government for statistics. |

| • | Copies of government documents. |

| • | Certificates of land value under PHP 200. |

| • | Lending and borrowing of securities through a registered exchange. |

| • | Loan agreements under PHP 250,000 for personal use. |

| • | Selling or trading shares on the stock exchange. |

| • | Assignments or transfers of mortgages, leases, insurance policies, or agreements if the terms don’t change. |

| • | Fixed-income securities traded on the stock exchange. |

| • | Derivatives (like repurchase agreements). |

| • | Loans between banks or quasi-banks that are due within 7 days. |

| • | Transfers of property under Section 40(C)(2) of the National Internal Revenue Code of 1997, as amended. |

| • | Contracts, deeds, documents, and transactions related to the Bangko Sentral ng Pilipinas. |

Documentary Stamp Tax (DST) Returns

Businesses and individuals engaged in transactions subject to DST are generally required to file DST returns and pay the corresponding tax. DST must be paid before or at the time of executing the document, and the payment must be reflected on the document itself.

Implications of Failure to Stamp Taxable Documents

| • | Non-Recordability: Documents that are not properly stamped cannot be recorded in government offices. |

| • | Inability to Use as Evidence: Unstamped documents cannot be used as evidence in court proceedings. |

| • | Notary Public Refusal: Notaries public are prohibited from acknowledging unstamped documents. |

Electronic Documentary Stamp Tax (eDST) System

| • | Purpose: The eDST system allows taxpayers to affix secure documentary stamps electronically using a computer and internet connection. |

| • | Requirements: To use eDST, taxpayers need a computer with a laser printer, internet access, and a compatible web browser. |

| • | Security Features: The eDST system incorporates security features, such as watermarks, to prevent fraud. |

DST Applicability to Electronic Documents

| • | DST applies to electronic documents: Electronic documents are considered equivalent to written documents under R.A. 9243 and R.A. 10963 and are therefore subject to DST. |

| • | Exemptions: Certain electronic documents may be exempt from DST, such as those specifically exempted by the Tax Code or its implementing regulations. |

Filing and Paying Documentary Stamp Tax Return

| • | When to File and Pay: You must file the return and pay the tax within 5 days after the document is signed or transferred. |

| • | Where to File and Pay: File the return and pay the tax at an Authorized Agent Bank (AAB) in the area where you live or where the property is located. |

| • | Payment Methods: You can pay in cash for amounts under PHP 20,000. For amounts over PHP 20,000, use a manager’s check or cashier’s check. You can also pay online using a bank debit, credit card, or mobile payment. |

| • | Proof of Payment: The bank will give you a receipt showing you paid the tax. You should also keep a copy of the return with the bank’s stamp. |

C. Local Taxes

Local taxes are taxes imposed by local government units (LGUs), such as cities, municipalities, and provinces. These taxes are an essential source of revenue for LGUs, used to fund local services and infrastructure. It can vary significantly from one municipality to another.

1. Real Property Tax

Real Property Tax (RPT) is a tax you pay on your land and any buildings on it. The amount you pay depends on the value of your property and where it’s located. Different cities and towns have different tax rates. You usually pay this tax once a year, but the exact date might vary.

How is RPT Calculated?

| • | Assessment: The local government assesses the fair market value of your property. This is based on factors like size, location, condition, and recent sales of similar properties. |

| • | Classification: Properties are categorized as residential, commercial, industrial, or agricultural. |

| • | Tax Rate: The tax rate depends on the property’s location and type. Cities and municipalities in Metro Manila generally have higher rates than those in provinces. |

| • | Calculation: The tax is calculated by multiplying the assessed value by the tax rate. |

Payment and Due Dates

| • | Annual Payment: RPT is typically paid annually. |

| • | Due Date: The exact due date varies by local government. Check with your local tax office. |

| • | Late Payment: If you don’t pay on time, you’ll face penalties and interest. |

Exemptions and Deductions

| • | Exemptions: Some properties might be exempt from RPT, like government properties or certain religious or charitable institutions. |

| • | Deductions: You might be able to deduct certain expenses from your taxable property value, like mortgage interest or property insurance. |

Delinquency and Foreclosure

| • | Delinquency: If you don’t pay your RPT on time, your property can become delinquent. |

| • | Foreclosure: If the delinquency continues, the government can sell your property to pay the tax. |

Online Services

Many LGUs now offer online services for RPT inquiries, payments, and returns. This can save you time and effort.

2. Local Business Taxes (LBT)

If you’re starting a business in the Philippines, you need to know about local business taxes. These taxes are collected by cities and towns.

Exemptions on Local Business Taxes

New businesses don’t have to pay the initial local business tax, but they still need to pay for a business permit and other fees.

Some businesses don’t have to pay local business tax. These include:

| • | New businesses registered with the Board of Investments (BOI) for 4-6 years. |

| • | Businesses that sell oil, gasoline, or other petroleum products. |

| • | Cooperatives registered with the Cooperative Development Authority. |

| • | Businesses registered with the Philippine Economic Zone Authority (PEZA). |

How is Local Business Taxes Calculated?

To calculate local business tax, businesses use their total income from the previous year. Only the money they actually received counts. This prevents double taxation.

Businesses can pay this tax once a year on January 20th or every three months on January 20th, April 20th, July 20th, and October 20th.

Local Business Tax Rates

The Local Business Tax (LBT) rates in the Philippines are determined by local government units (LGUs) through their respective ordinances. The municipality may impose taxes on various businesses with gross sales or receipts for the preceding calendar year based on the provisions stated under Section 143 of the Local Government Code of the Philippines.

3. Community Tax

The community tax, also known as the residence tax or cedula, is a tax imposed on individuals and corporations residing or doing business within a municipality.

Who is liable for Community Tax?

Everyone in the Philippines who is 18 or older must pay community tax. This includes people who have a job, own a business, own property worth at least PHP 1,000, or are required to file income tax.

Basic Community Tax

| • | Individuals: The basic community tax for individuals is PHP 5.00. |

| • | Corporations: The basic community tax for corporations is PHP 500.00. |

Additional Community Tax

| • | Individuals: An additional community tax of PHP 1.00 is imposed for every PHP 1,000.00 of gross income derived from employment, business, or property. The maximum additional tax for individuals is PHP 5,000.00. |

| • | Corporations: The additional community tax for corporations is based on the assessed value of their real property and the gross receipts or earnings derived from their business operations. The maximum additional tax for corporations is PHP 10,000.00. |

Exemptions

| • | Diplomatic and consular representatives |

| • | Transient visitors with a stay of less than three months |

| • | Certain individuals and corporations are exempted by specific laws or ordinances. |

When and How to Pay Community Tax

| • | Payment Place: Pay the tax where you live or where your business is located. |

| • | Due Date: You must pay the tax by the end of February each year. If you turn 18 or lose your tax exemption after June 30th, you have 20 days to pay. |

| • | New Residents: If you move to the Philippines or turn 18 after June 30th, you don’t need to pay the tax for that year. |

| • | Corporations: Corporations established before June 30th must pay the tax for that year. If established after June 30th, they don’t need to pay for that year. |

| • | Late Payment: If you don’t pay on time, you’ll pay a 24% interest penalty each year until you pay the tax. |

The Philippine tax system is complex, encompassing a wide range of taxes that contribute significantly to government revenue. Adherence to tax laws is essential for maintaining a fair and equitable tax environment.

Key Takeaways

| • | Tax Compliance: Ensure accurate and timely tax filings to avoid penalties and interest. |

| • | Professional Guidance: Seek advice from qualified tax professionals to navigate the complexities of the tax system effectively. |

| • | Tax Planning: Implement strategic tax planning to minimize tax liabilities and optimize financial outcomes. |

| • | Stay Informed: Stay updated on tax law changes and developments to make informed decisions. |

To make sure you’re paying the right amount of tax, regularly review your tax situation and consider getting help from a tax professional. Stay up-to-date on tax changes by subscribing to HousingInteractive’s newsletters or following tax news. By paying your taxes correctly, you contribute to the development of the Philippines.